Since our second quarter forecast, our projected rise in mortgage rates has occurred and accelerated, as the Bank of Canada—spurred by economic growth that far exceeded its outlook—turned suddenly hawkish. The Bank surprised with a 25-basis point increase in July and then again in September, taking its overnight rate back to 1 per cent, where it was before the precipitous drop in oil prices that shocked the Canadian economy in 2014. After the July interest rate hike, markets widely expected at least one additional rate increase in the fall, and so bond markets and lenders had already priced in the September increase by the time it occurred.

Since our second quarter forecast, our projected rise in mortgage rates has occurred and accelerated, as the Bank of Canada—spurred by economic growth that far exceeded its outlook—turned suddenly hawkish. The Bank surprised with a 25-basis point increase in July and then again in September, taking its overnight rate back to 1 per cent, where it was before the precipitous drop in oil prices that shocked the Canadian economy in 2014. After the July interest rate hike, markets widely expected at least one additional rate increase in the fall, and so bond markets and lenders had already priced in the September increase by the time it occurred.

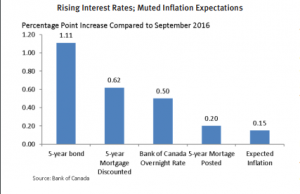

Over the past 12 months, the 5-year bond yield has risen 110 basis points to a three-year high of close to 1.8 per cent, prompting a 60-basis point increase in 5-year discounted mortgage rates to above 3 per cent for the first time since 2014. The 5-year qualifying rate has risen just 20 basis points to 4.84 per cent. The latter is an interesting development, because it is the first increase in the posted rate since stricter qualifying rules for insured mortgages were imposed last fall. Rising mortgage rates may complicate the introduction of further mortgage qualifying restrictions slated for October, this time tightening lending for uninsured mortgages.

We anticipate that the Bank of Canada will hold off on further rate increases this year and assess how higher rates are impacting the economic and inflation outlook. However, in the Bank’s recent communications, it has very clearly left the door open for more aggressive tightening should the current torrid pace of economic growth continue. Our baseline forecast is for the 5-year fixed mortgage rate offered by lenders to average 3.15 over the fourth quarter, eventually rising to 3.44 by the end of 2018. The posted 5-year qualifying rate is forecast to reach 5.14 per cent by the end of next year.

For the complete news release, including detailed statistics, click here.